Stock Price Prediction using Machine Learning

Objective

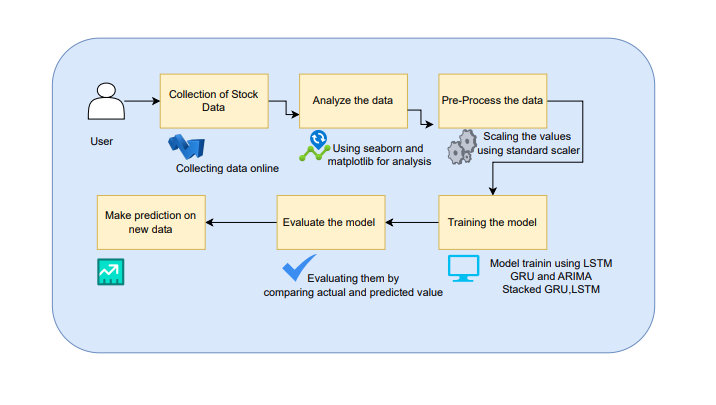

The project enhances stock price prediction accuracy by comparing traditional models with advanced techniques like LSTM, GRU, and ARIMA, aiming to minimize MSE and improve forecasts.

Abstract

This project explores stock price prediction using machine learning techniques to improve forecasting accuracy. We evaluated traditional algorithms such as Random Forest Regressor and Support Vector Regression (SVR), which yielded Mean Squared Errors (MSE) of 85.57 and 2878.20, respectively. To enhance performance, we implemented advanced models including Long Short-Term Memory (LSTM) networks, Stacked LSTM, Gated Recurrent Units (GRU), and Stacked GRU, alongside the Autoregressive Integrated Moving Average (ARIMA) model. The LSTM and its stacked variant achieved validation losses of 0.5048 and 0.9658, while the GRU and Stacked GRU models demonstrated even better results with validation losses of 0.0101 and 0.0361, respectively. ARIMA also performed notably well, with a Mean Squared Error of 11.86. The dataset utilized comprises 2417 entries with features including Adj Close, Open, High, Low, Close, and Volume. These results indicate significant improvements in prediction accuracy with the proposed models.

Keywords: Stock price, Machine learning, LSTM, GRU, Mean square error, Forecasting Stock.

NOTE: Without the concern of our team, please don't submit to the college. This Abstract varies based on student requirements.

Block Diagram

Specifications

H/W CONFIGURATION:

Processor - I3/Intel Processor

Hard Disk - 160GB

Key Board - Standard Windows Keyboard

Mouse - Two or Three Button Mouse

Monitor - SVGA

RAM - 8GB

S/W CONFIGURATION:

• Operating System : Windows 7/8/10

• Server side Script : HTML, CSS, Bootstrap & JS

• Programming Language : Python

• Libraries : Flask, Pandas, MySQL. Connector, Tensor flow, Keras

• IDE/Workbench : VS Code

• Technology : Python 3.8+

• Server Deployment : Xampp Server

Paper Publishing

Paper Publishing

Request Call Back

Would you like to receive a free callback now?

Choose the best time for callback:

Leave your message and we will contact you as soon as possible

6-2-85/B, Old Maternity Hospital Road, Thyagaraja Nagar, Tirupati, Andhra Pradesh – 517501

+91 9030333433

+91 9393939065

0877-2261612

Disclaimer - Takeoff Edu Group Projects are not associated or affiliated with IEEE in any way. The IEEE Projects mentioned here are mentioned in the context of student projects, whose ideas are derived from IEEE publications, not projects of or by IEEE.