Deep Learning for College Graduates Employment Prediction A Computational Approach

Objective

This project develops an intelligent financial risk prediction and debt management system using machine learning, ensemble learning, and hybrid models to identify customers with high default or delayed payment risk. The framework integrates Random Forest, Decision Tree, ASFWE(Adaptive Stacked Feature-Weighted Ensemble), and an Autoencoder-Tree Hybrid model to analyze customer demographics, payment history, and usage behavior. Advanced preprocessing and ensemble techniques improve prediction accuracy, robustness, and financial decision-making. The system enables early risk detection, optimized debt monitoring, and proactive collection strategies for telecommunications providers.

Abstract

This project presents a machine learning framework for predicting financial risk and optimizing debt management in the telecommunications sector. The framework integrates Random Forest, Decision Tree, Adaptive Stacked Feature-Weighted Ensemble (ASFWE), and an Autoencoder-Tree Hybrid model to capture complex patterns in customer demographics, usage behavior, payment history, and socioeconomic factors. The dataset undergoes preprocessing steps including data cleaning, feature engineering, outlier detection, and normalization to ensure robust model training. Random Forest and Decision Tree models identify nonlinear relationships in customer data, while ASFWE leverages stacked ensembles with feature weighting to enhance predictive performance. The Autoencoder-Tree Hybrid captures latent representations of customer behavior, providing a nuanced understanding of risk factors. The system classifies customers according to their likelihood of default or delayed payment and evaluates multiple scenarios to support strategic financial decisions. Experimental results demonstrate that ensemble models outperform individual models in accuracy, F1-score, and robustness. This framework offers telecommunications providers a scalable, explainable, and proactive decision-support tool for debt monitoring, enabling early risk detection, improving collection strategies, and enhancing overall financial resilience.

Keywords: Financial Risk, Debt Management, Telecommunications, Random Forest, Decision Tree, ASFWE, Autoencoder-Tree Hybrid, Ensemble Learning, Predictive Analytics, Scenario Modeling.

NOTE: Without the concern of our team, please don't submit to the college. This Abstract varies based on student requirements.

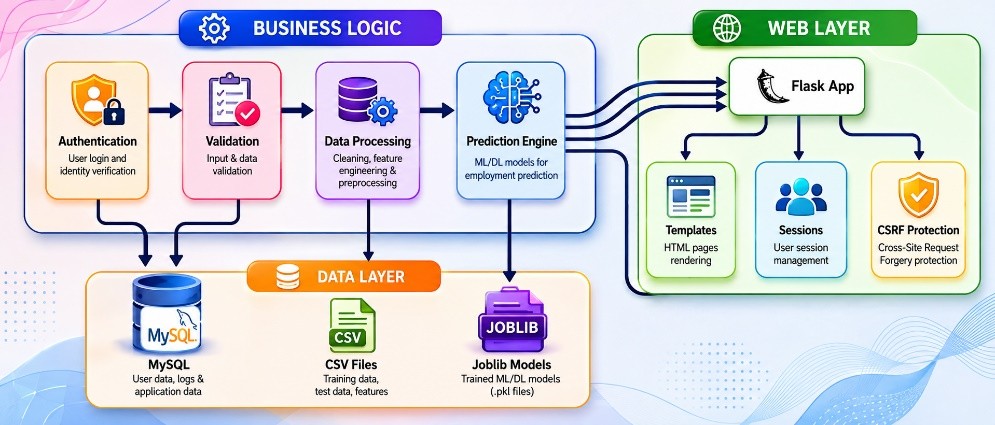

Block Diagram

Specifications

4.1 SOFTWARE REQUIREMENS

Operating System : Windows 7/8/10

Server side Script : HTML, CSS, Bootstrap & JS

Programming Language : Python

Libraries : Flask, Pandas, Sklearn, Numpy , Seaborn

IDE/Workbench : VSCODE

Server Deployment : Xampp Server

Database : MySQL

4.2 HARDWARE REQUIREMENTS

Processor - I3/Intel Processor

RAM - 8GB (min)

Hard Disk - 128 GB

Key Board - Standard Windows Keyboard

Mouse - Two or Three Button Mouse

Monitor - Any

Paper Publishing

Paper Publishing

Request Call Back

Would you like to receive a free callback now?

Choose the best time for callback:

Leave your message and we will contact you as soon as possible

6-2-85/B, Old Maternity Hospital Road, Thyagaraja Nagar, Tirupati, Andhra Pradesh – 517501

+91 9030333433

+91 9393939065

0877-2261612

Disclaimer - Takeoff Edu Group Projects are not associated or affiliated with IEEE in any way. The IEEE Projects mentioned here are mentioned in the context of student projects, whose ideas are derived from IEEE publications, not projects of or by IEEE.